- Hardware

- A

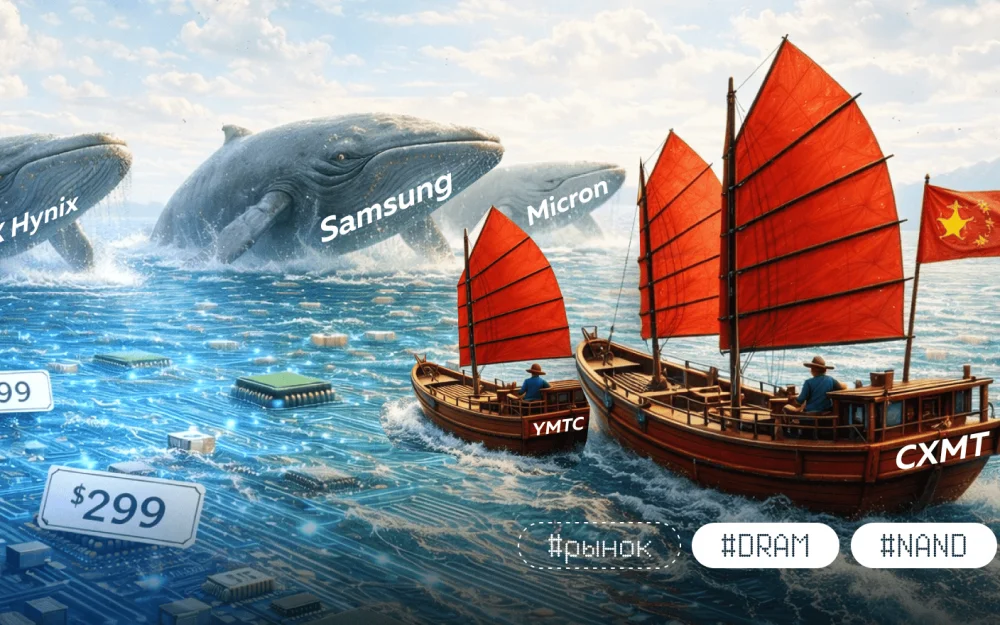

Impact of Memory from China on Prices in 2026–2027: A Look at CXMT and YMTC

It seems that the entry of Chinese CXMT and YMTC into the memory market is a solution to rising prices. But when looking at the numbers, only three companies control over 90% of the DRAM market, with Chinese players holding only a small share. This article examines what Chinese manufacturers can actually do, why "cheap memory from China" is a myth, and what this means for those building IT infrastructure in Russia.

It seems that the entry of Chinese CXMT and YMTC into the memory market is a salvation from rising prices. But if we look at the numbers, just three companies control more than 90% of the DRAM market, and Chinese players account for only a small share. In this article, we analyze what manufacturers from the Middle Kingdom can really do, why "cheap memory from China" is a myth, and what it means for those building IT infrastructure in Russia.

Why are we discussing this at all

All market participants have already felt the rise in memory prices in 2025-2026 (we have already done a detailed analysis of the dynamics). The main driver of the current shortage is the AI infrastructure boom.

We at mClouds.ru, when introducing new equipment in our cloud platform, both with GPU and without, have already seen price increases for DDR5 RDIMM in supplies, but prices for the cloud itself for customers remain unchanged, as we purchased significant volumes of modules back in 2025.

Memory manufacturers since 2025 have been actively reallocating capacities toward high-margin products: enterprise SSDs and HBM for GPU accelerators. As a result, "regular" memory takes a back seat, and the largest contract manufacturers book volumes first, leaving other buyers with leftovers at high prices.

CXMT positions itself as a full-fledged challenge to the "Big Three": Samsung, SK Hynix and Micron. In its presentations, CXMT claims support for DDR5 up to 8000 MT/s, LPDDR5X standards, and has server RDIMM/MRDIMM modules in its portfolio. It seems like CXMT is ready to add a lot of affordable memory to the market tomorrow. In February, the company started selling a 32GB DDR4-3200 ECC server memory module at a price of $138 — two to three times cheaper than the market average.

But according to industry insiders, the key problem for CXMT is the yield of good chips for DDR5. It remains at just above 50%. For the mass market, this is low: low yield means high cost and the physical impossibility of quickly scaling volumes. This is precisely what is holding back the promised mass production. Plus, it is important to consider CXMT's actual share of the DRAM market, which is about 4-5% of the global market.

What does this mean?

If experts’ expectations come true and by 2027 CXMT’s share of production capacity rises to 11–15%, the company will become an important source of additional volumes within China and through parallel import channels. But it is not worth expecting CXMT to become a player capable of dumping prices.

YMTC: Technologically strong but externally vulnerable

Technologically, the company looks very solid: YMTC produces chips with 232 active layers of 3D NAND and uses its proprietary Xtacking architecture. This allows it to achieve densities and speeds comparable to market leaders.

At the beginning of March, the company announced the PC550 — its first consumer M.2 PCIe 5.0 solid-state drive with NVMe 2.0 protocol support. Its maximum sequential read speed reaches 10,500 MB/s, and write speed — 10,000 MB/s. The memory is available in capacities of 512 GB, 1 TB, and 2 TB.

However, for an infrastructure customer, peak performance is less important than supply stability. Here, YMTC faces restrictions on access to equipment and service. Since the end of 2022, the company has been on the Entity List — a registry of the U.S. Department of Commerce that strictly limits the export of technologies and equipment. This creates production risks: it becomes harder to service lithography machines, longer to wait for spare parts, and more difficult to upgrade production lines. As a result, the company can create an excellent chip but cannot guarantee large-scale supply volumes for years.

What does this mean?

YMTC is a source of affordable SSDs that show decent speed and often win on price. At the same time, the company’s share of the global market is actively growing and could reach 15% by the end of 2026, but this is still just a forecast; the actual dynamics will become clear in the second half of the year. However, long-term guarantees of stable supply for specific models from YMTC may currently be lower than those of global vendors.

Why “Chinese memory” hasn’t become cheap even in China

There is a persistent myth: “If you buy memory directly in China, it will be cheaper.” The logic is understandable: remove intermediaries, get the product from the source. However, reality shows the opposite: prices in Chinese retail have equalized with European and American prices, and sometimes even exceed them. To understand why, let’s look at the pricing structure.

The memory market is heterogeneous, and the price depends on who and how the purchase is made:

Spot — the price here and now. This is an indicator of scarcity for traders. The most volatile layer: today the price is one thing, tomorrow it's 10% higher.

Contract — the price for long-term agreements for large buyers. Usually more stable, but during periods of acute scarcity, like now, it is reviewed quarterly in the direction of growth. This level determines the cost price for the industry.

Retail — the final price for the user. It consists of the following components: contract base + module assembly + logistics + taxes + channel margin.

If memory in China becomes significantly cheaper than globally, the arbitration mechanism kicks in: traders buy up the volume and send it to where the prices are higher — Europe, the USA, Russia. This flow equalizes the spread: cheap memory disappears from the local market, and the price rises to the global level. This is why "cheaper in China" does not mean "the world will get cheaper." Global prices are dictated by the volumes and contracts of the "Big Three," and retail simply follows them.

If global contract prices rise, this inevitably affects retail everywhere, including China. That is, substantial savings from parallel imports from China can only be achieved on a case-by-case basis, but not systematically. The new reality is high cost per gigabyte, regardless of the purchase geography.

Can Apple switch to Chinese memory?

Recently, news surfaced that Apple is considering using memory chips from YMTC and CXMT in its devices. For the market, this is a strong signal: if a technological giant of this level considers an alternative, it means the quality has improved. However, from an infrastructure standpoint and its impact on global prices, the situation is not so clear-cut. There are problems:

Technical barriers to integration. For Apple, memory is not just a separate chip on the board. In iPhone and iPad, LPDDR chips are often integrated into a single package with the processor. This requires the highest level of qualification not only from the memory manufacturer but also from the assembler. Any new supplier must undergo a lengthy qualification procedure: checking thermoprofiles, signal compatibility, and soldering reliability. This is engineering work for years.

Volume and yield of functional chips. Apple purchases memory in volumes that constitute a significant share of global production. CXMT, even with growth, occupies about 4% of the global DRAM market. At the current yield level for complex standards like DDR5, it is difficult to meet the demands of such a giant without risks to stable deliveries.

Reliability and precedents. It is important to remember the history of the issue: back in 2022, there were reports of a pause in Apple's plans to use YMTC chips. The reason was the requirements for the predictability of the supply chain. For a vendor of Apple's level, it is critical to guarantee the production of millions of devices without delays. Until Chinese manufacturers prove the stability of mass production over the long term (3–5 years), a switch is unlikely.

If the deal goes through, it is important to understand: Apple's consumption volumes are so large that they will likely "take" the available Chinese resource into their closed supply chain—and prices will only rise. If the cooperation remains at the rumor level, cheap chips are still not to be expected: low prices will quickly be leveled out by arbitration.

Where China can really help and where it almost can’t

Segment | Potential impact of CXMT and YMTC | Why |

DDR5 UDIMM (PC) | Moderate, through retail / export of modules | Large OEMs select available volumes based on their contracts, Chinese brands often mix chips |

DDR5 RDIMM/MRDIMM (servers) | Limited | Guarantees, qualification, and compatibility are required. The path to global platforms is long |

NAND/SSD | Higher than in DRAM | There are more players, some brands are third-party manufacturers. However, sanctions + the priority of corporate SSDs prevent a "price crash" |

CXMT and YMTC are "alternatives with caveats." Their influence is noticeable where the entry barrier is lower: DIY builds, workstations, test circuits. In critical infrastructure (server clusters, HBM systems), CXMT and YMTC are not yet replacing the "Big Three," but merely complementing them.

Scenarios for 2026–2027: What to expect and how it will impact IT budgets

We identified three market development scenarios, based on the production plans of the leaders and the real capabilities of CXMT and YMTC.

Optimistic: "Slowing price growth". Demand from AI projects will normalize, hyperscalers shift from panic bookings to planned purchases. New capacities, such as Micron’s factory in Singapore, are starting to prepare deliveries for 2027. CXMT successfully solves problems with producing viable DDR5 chips and increases mass shipments.

Price growth slows, and certain consumer categories may slightly "revert" after peaks. However, there will be no return to the levels of early 2025: the market has already adapted to the high margins of AI.

Base: "Stable high prices" — most likely. Demand-supply imbalance persists. Manufacturers' priority is high-margin HBM and corporate SSDs. CXMT and YMTC add volume, but mostly within China and through limited export channels. YMTC operates within restrictions, while CXMT remains in the DIY and consumer device niche due to difficulties with server qualification.

Server memory and enterprise SSDs remain the most sensitive and expensive segments. Consumer DDR5 is stabilizing, but at high levels (as we are seeing now in EU and China retail).

Stress scenario: "availability gap." Tightening of export restrictions on equipment and services for Chinese fabs. A new wave of AI reservations from global players. CXMT faces regulatory barriers or does not scale DDR5 production. YMTC experiences difficulties servicing lines due to sanctions.

Contract prices jump sharply from quarter to quarter. In retail — availability gaps. Server commodity items are becoming more expensive faster than consumer ones.

Summing up all three scenarios, let’s be clear: CXMT and YMTC in 2026–2027 will not be the trigger that collapses memory prices. These companies are an important buffer for availability and technological progress, but not a tool for global dumping. That is why we should not expect a return to early 2025 prices.

Infrastructure planning should be based on the new reality: high cost per gigabyte, long procurement cycles, and the need for standardization. CXMT and YMTC will help weather acute shortage phases, but they will not change the rules of the game.

Which scenario seems most likely to you? What are you already doing to adapt? Share in the comments.

![From Virtual Hands to AI for Survivalists: Curious Open Agent OSes [and One Hardware Project]](https://cdn.tekkix.com/imgs/2026/05/habrcom/big/ce0b1057616faed51cd8b9f3b2b9.webp)

Write comment