- AI

- A

Why AI Is Not a Dotcom Bubble

The reduction in technology costs means widespread adoption, not a decline.

Cheaper technology means ubiquity, not decline.

For more than a year now, from every possible source – friends and family to my X feed and YouTube videos – I’ve been hearing the same thing: the AI boom is about to burst like the dot-com bubble. Company valuations seem insane, everyone keeps repeating it, and there’s this persistent feeling of “too good to be true.” I understand where such comparisons come from. But I am convinced that they are fundamentally wrong, and the difference here is much more significant than commonly believed.

While everyone debates whether Nvidia’s stock is overvalued, the real economic threats quietly hide in the shadows of these discussions.

Look at the numbers, and the resemblance disappears

The dot-com crash happened because many firms had nothing behind them except empty promises. Pets.com sold dog food at a loss. Webvan promised grocery delivery that never became profitable, and some projects were outright scams. When reality knocked on the door, the Nasdaq index fell 78% between 2000 and 2002.

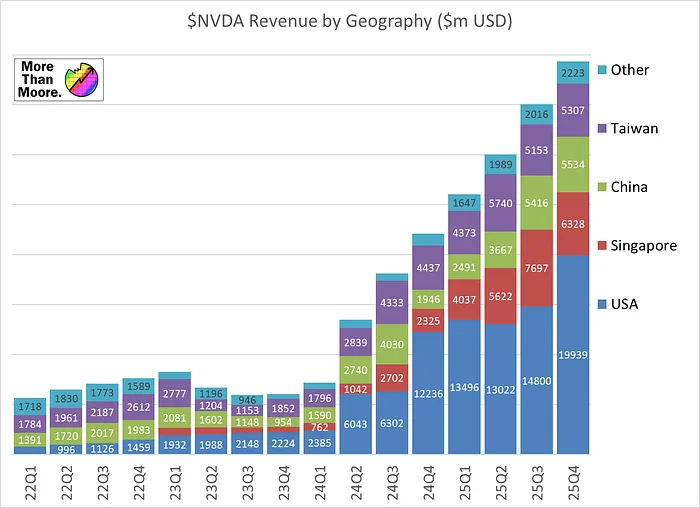

Today’s AI giants are birds of a very different feather. In fiscal 2025, Nvidia reported revenue of $130.5 billion – 114% higher than the previous year, with operating profit of $81.5 billion. In the most recent quarter, revenue reached $57 billion (up 62% year-on-year), and on an annual basis the company is confidently approaching $200 billion. Revenue from the data center segment alone amounted to $115.2 billion for the fiscal year, showing 142% growth.

These are not empty startups burning venture capital in the hope of eventually finding a business model. Cloud providers are already making significant revenue from AI services. Microsoft’s Azure, Google Cloud, and Amazon’s AWS – all of them generate real cash flow, charging corporate clients for computing power. The infrastructure exists. The clients are in place. The product works. In 1999, no “average” dot-com era company could have dreamed of such a scenario.

Can stock market quotes detach from reality? Of course, that's the nature of the market. Can some AI startups with zero revenue crash to nothing? Undoubtedly. But comparing it to a bubble built on fictitious reporting and empty accounts just doesn't hold up. Even if every first AI startup closes tomorrow, Nvidia will still have its 130.5 billion in revenue. Data centers won't disappear. Chips are physical hardware that will continue processing data. All that remains of Pets.com is a puppet sock from the commercial and a warehouse full of unsold dog beds. That’s the difference.

The Jevons Paradox: Why Cheap AI Means More AI, Not Less

Here lies the main reason why I believe the current boom is not a speculative frenzy, but a deep structural shift.

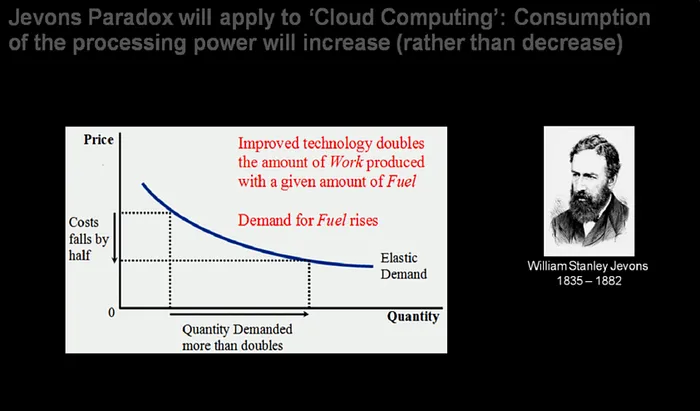

In 1865, William Stanley Jevons noticed a curious thing about coal. When James Watt made steam engines more efficient, everyone assumed that Britain would need less coal. The exact opposite happened: consumption skyrocketed. The reduction in the cost of energy per unit of work made steam engines available to many factories. As a result, more coal was burned overall, not less. Efficiency did not reduce demand—it released it.

This is exactly what we are seeing now with the cost of inference (the work of ready-made models). The Vera Rubin platform from Nvidia (introduced at CES 2026 and already in production) offers a tenfold reduction in token cost compared to the Blackwell architecture. The speed of operation increased fivefold, and training the same models now requires four times fewer GPUs!

Naive view: "Great, now we will need fewer chips." View through the lens of Jevons: "Inference became 10 times cheaper, which means that tasks that were previously unaffordable now suddenly make sense." Specialized internal tools, micro-automation, AI agents for complex workflows, vibe coding, where a person simply describes the task, and the agents assemble it. Each new application creates constant demand for inference. The cost of one token drops, but the total token consumption shoots up into the stratosphere.

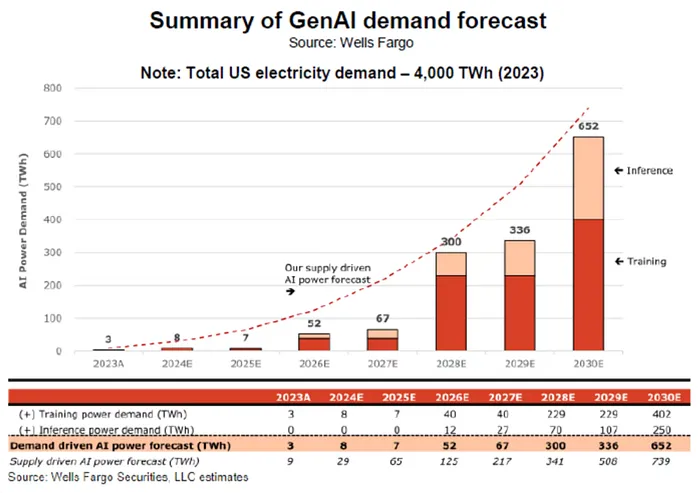

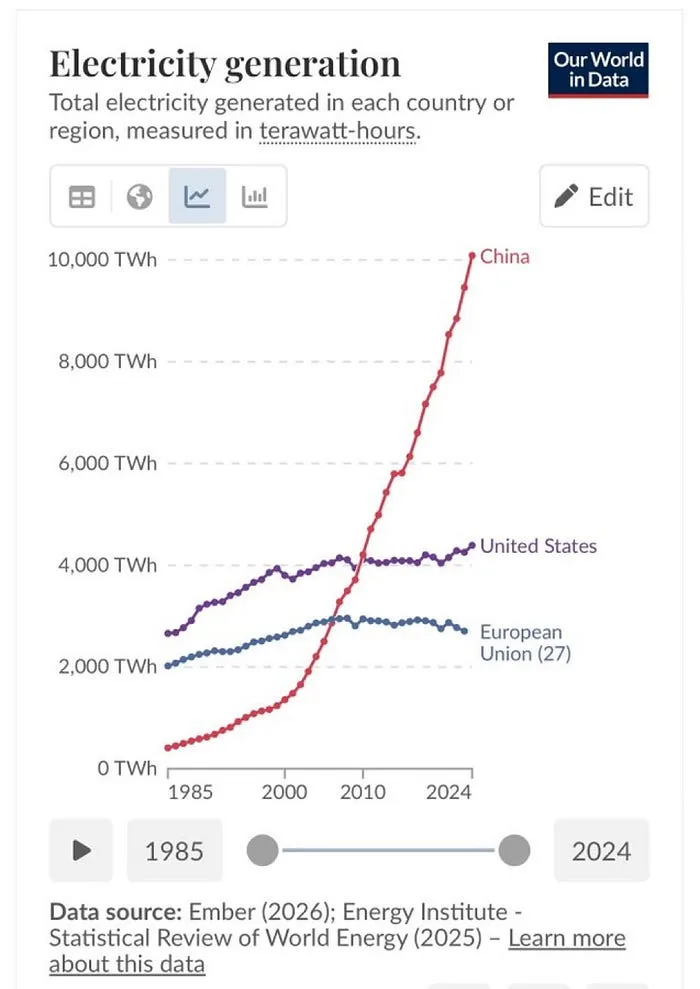

And these are not empty theories. According to JLL's 2026 Global Data Center Outlook forecast, the capacity of data centers worldwide will reach about 103 GW by the beginning of 2026, with AI accounting for about 25% of it. By 2030, the capacity is forecasted to double to 200 GW, with the share of AI growing to 50%. The compound annual growth rate of 14% in capacity is not the result of speculative bets. It is a response to real and growing demand. JLL itself summarizes: "Real estate market indicators do not suggest a bubble." Global capacity occupancy is 97%, and 77% of the construction projects are already reserved by tenants.

We’ve seen similar processes in other industries. What was once a supercomputer the size of a workshop is now in the pocket of an average resident of a developing country. Chinese BYD is squeezing out the auto industries of Europe and the USA by producing cheap electric cars that are rapidly improving and costing less than internal combustion engine vehicles. Personal computers, Henry Ford – all of them started with customers that were overlooked by the market leaders of the time. The curve of cost reduction and mass production did the rest. Humanity has already witnessed such transformations live. The same dynamic is here. AI does not just replace the existing market – it creates a new, much larger layer beneath it, which expands as technology becomes cheaper.

Jevons' Paradox in action. The author rightly notes: the cheaper inference becomes, the more tasks we are willing to load onto it. This is why access to different models is not a luxury, but a necessity for those who want to be at the forefront. BotHub provides the opportunity to experiment with top-tier neural networks (GPT-5.4, Claude 4.6, Gemini, and others) in one window, without overpaying for individual subscriptions.

Analogy with the Printing Press

In my opinion, the closest historical analogy to what is happening now is not the dot-com boom, but the invention of the printing press.

Before Gutenberg, reading and writing were the domain of the chosen few – a narrow caste of intellectuals serving the church or kings, who, by the way, were often illiterate themselves. Copying a book by hand took months. Access to information was blocked by a "bottleneck" – the enormous labor intensity of the process. But the printing press came along, turning text reproduction into a cheap endeavor, and in just one generation, literacy levels skyrocketed. New forms of knowledge production emerged, which no one could have imagined before. And the people who previously copied books by hand did not remain idle. They became researchers, editors, translators, and scholars, whose work became exponentially more productive because that very obstacle disappeared.

What we are witnessing in the software and intellectual labor field today is essentially a world on the eve of the printing press. An elite skill is becoming the property of the masses. Even without any AI, the tasks I was able to automate using bash scripts, APIs, and webhooks made me slightly more efficient than most ordinary office workers. And it wasn’t that I was smarter; it was that I had access to tools that had existed for decades but were too obscure and complex for most people.

Now tools like Claude and Cursor provide these capabilities even to my parents – through future versions of Siri on their phones.

The printing press did not deprive great scientists of their jobs. It made their work more productive and sparked an unprecedented surge of human creativity, the fruits of which became accessible to everyone. It is likely that the same will happen with AI.

AI as a Deflationary Machine

For many years, a chart has been circulating online that clearly shows the gap in consumer prices in the US. Over the past two decades, the cost of industrial goods (televisions, clothing, software, toys) in real terms has plummeted thanks to globalization and automation. At the same time, prices for services that require live human labor (healthcare, education, housing, insurance, childcare) have soared through the roof.

The pattern is obvious: everything that can be outsourced or automated becomes cheaper. Everything that requires the presence of a live person at a specific place and time becomes more expensive. The entire current cost-of-living crisis in the US is a story about sectors where labor costs cannot be reduced.

Artificial intelligence is changing the rules of the game. Not by replacing doctors and teachers entirely, but by making each of them much more effective. I currently work in healthcare. We are desperately short of radiology technicians to cover all shifts in all clinics. But AI-driven diagnostics do not eliminate the need for a person. It makes examinations cheaper and more accessible to a greater number of medical institutions, which in fact only increases the demand for qualified specialists. The human remains connected to the patient – for decision-making, for medical judgment, for everything that requires hands and eyes in the office. AI takes on the role of the "gatekeeper", eliminating bottlenecks in data processing.

By 2030, the baby boomer generation will be retiring at a rate of 4 million people per year. This is the largest and longest exodus from the workforce in U.S. history. Without a sharp rise in productivity to offset the declining number of workers, service-sector inflation will accelerate, social security and healthcare costs will balloon, and the entire financial system will be strained to the breaking point. AI is one of the few significant counterweights to this relentless demographic arithmetic.

What AI will not do

I do not harbor utopian illusions. Any tool by itself is devoid of morality – choices are made by the people who wield it.

The development of large language models (LLMs) will sooner or later hit a “plateau” according to the Pareto principle. The growth rates that seem exponential today will eventually slow down. AI will become the foundation for other innovations, but some of them will have to wait until a different intelligence structure emerges, until energy production catches up with demand, or until some other obstacle is removed. The combination of technologies is more important than each of them individually. The massive mylar balloon satellites, which Bell Labs used to reflect radio waves, were only the first tentative steps, paving the way for the real Telstar to fly. But for Telstar’s success, not only the satellite idea was needed, but also other inventions – for example, solar panels.

It will not be painless. Most likely, we are on the brink of an industrial revolution for white-collar workers, and we can expect upheavals comparable to the struggles of artisans against industrialists, perhaps with accompanying chaos. But looking at the big picture, people’s lives will become noticeably better: higher-quality healthcare, broader opportunities. This is exactly what industrialization did with food: it became so accessible that 90% of farmers lost their jobs, but most people stopped going hungry.

The main law of economics, often forgotten in such debates: human desires are limitless. People are only prevented from obtaining what they want or need by a lack of resources and money. Industrialization made food accessible. Globalization – industrial goods. AI will most likely do the same with the things we can imagine today, and with those we cannot even yet conceive of.

Think of a person born in 1890. Could they have imagined that in their lifetime people would land on the Moon? Or at least the rise of low-cost carriers like RyanAir?

The real risks are hiding somewhere else

If the AI boom does not pose an existential threat, then where is the real threat?

I discussed this in detail in the article "The Load-Bearing Wall": this includes the $3.5 trillion private credit market, which is gambling with pension funds; the collapse of private equity buyout schemes amidst the normalization of interest rates; and the $265 billion market capitalization that evaporated overnight for alternative asset managers. Structural risks undermining the economy arose ten years before any AI. Post-COVID consumer fatigue, stagnation of real wages in the service sector, the "extend and pretend" policy in private equity, inflated by cheap money during the pandemic, as well as the housing market deficit in China and the crisis of overproduction – none of these problems were caused by artificial intelligence. On the contrary, the incredible successes of the AI sector partially mask these gaps, and blaming AI for the economy seeming "broken" is like confusing the symptom with the diagnosis.

"Vibe-recession" – when numbers seem normal, but people feel uneasy – is quite real. GDP growth is now supported by three pillars: government spending, healthcare, and investments in technology. The rest of the economy – the one most of us live in – grows by barely 1%. AI is one of the supports that keeps the overall indicators from falling, not something that drags them down.

If AI takes over bureaucratic tasks in healthcare and insurance, becoming a reliable assistant to doctors, it will reduce one of the fastest-growing expenses for the population. And this will not lead to mass layoffs. The population is aging and consuming more and more healthcare services. Automation will allow staff to focus on direct communication with patients instead of filling out endless forms and reports, which inflate overhead costs to billions.

If AI helps developers build affordable housing faster and cut through the bureaucratic thickets, or construct high-speed highways (which in reality is limited not by a lack of concrete, but by piles of approval documents) – that is an economy working for the benefit of people. Reducing labor costs in the consumer services sector will be a true blessing for all of us.

In my view, the recent work by Citrini Research practically ignores Jevons’ paradox. They model the impact of AI as a linear displacement process: technology improves, workers are laid off, incomes fall, and a recession follows. But this is too simplistic, a naive approach. The economic “pie” will grow, not just be redistributed. And even if it doesn’t grow as rapidly as optimists hope, AI is already offsetting declines in sectors that began contracting even before its arrival. If we trust Jevons’ lessons, cheap AI will create new use cases, new demand, and new kinds of activities. The printing press didn’t destroy the market for ideas on paper – it created a new market, which turned out to be millions of times larger than the old one.

Are we in for a correction in AI company valuations? Absolutely. Corrections are a normal market mechanism. But comparing this to 1999 is to confuse a temporary price drop with a structural collapse. The dot-com crash showed that behind inflated price tags there was emptiness. A correction in AI will show that behind the numbers lies reality: $130 billion in revenue for Nvidia, profitable cloud services, physical infrastructure, and deflationary technology that the aging developed world needs as much as air.

The question is not whether stock prices will fall. They will. The question is whether the created infrastructure will survive and whether productivity growth will continue. In 1999, telecommunications giants were collapsing, but the fiber optic cables remained in the ground. The internet infrastructure outlasted the companies that overpaid for its creation. This time, the builders are those who were forged in the fire of 1999. They are not risking other people's venture capital – they are investing their own enormous profits. Nvidia, Microsoft, Google, Amazon – these are not Pets.com with bare ambitions.

![From Virtual Hands to AI for Survivalists: Curious Open Agent OSes [and One Hardware Project]](https://cdn.tekkix.com/imgs/2026/05/habrcom/big/ce0b1057616faed51cd8b9f3b2b9.webp)

Write comment